Our industry is undergoing a period of transformation. From evolving technology capabilities to the complexities of organisational models, change is here.

We have identified five fundamental changes to the industry which will be increasingly prevalent and important for brands, agencies and marketing teams:

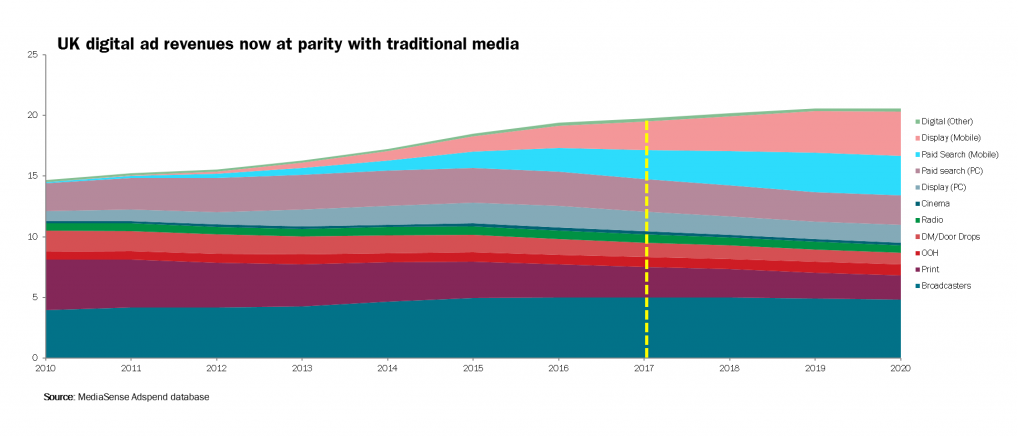

ONE: Technology & data are changing the media ecosystem

“Marketing teams which own and activate their own customer data are driving change within their organisation, and are more likely to secure the investment to build out their teams, resources and internal capability.”

Ownership and activation of data in-house – aided by technology – is now seen as a prerequisite for brands. This charge is led by the C-Suite who believe that in-house ownership of 1st party data is mandatory for success.

By controlling data, brands can achieve greater oversight of the customer journey, which in turn means marketers are more informed and their results more accountable. Accordingly, marketers are becoming more influential and empowered in the boardroom, as they are better able to demonstrate marketing’s capability as a lever for business growth.

Marketing teams which own and activate their own customer data are driving change within their organisation, and are more likely to secure the investment to build out their teams, resources and internal capability.

TWO: Customer-centricity is encouraging new organisational models to emerge

Brands have been undergoing organisational change and are reconfiguring around data capabilities – data management, data modelling & data activation, and are seeing the benefits.

To manage customer data in-house, a customer-centric model requires brands to organise teams differently with increased and diverse specialisms. We believe agile ways of working will continue to increase, with linear processes demonstrably inadequate to achieve the speed, fluidity and flexibility to work across production, resources, organisation, collaboration, development, creativity needed for this evolving way of working. On this basis, the traditional practice of orchestrating multiple agencies and specialists is becoming increasingly difficult and self-limiting.

Four organisational strategies are emerging:

- Best-of-Breed

- Holding Company

- In-House agency (owned)

- On-site agency (rented)

But these are by no means the only brand/agency models, and many brands are operating a hybrid model as they transition from legacy to customer-centric ways of working. By way of example, you can rent programmatic capability but “own” the people; or you can “rent” the people but own the programmatic capability. The increase in brands seeking alternative counsel or changing operating models should be a cause for concern for media agencies, especially with the emergence of new ways of working and the technology platforms.

THREE: Visibility within the media supply chain is the overriding concern

In a data-driven world, transparency is not just limited to clients seeing where the money flows, it’s also about seeing where your content is going.

Full-disclosure should be a non-negotiable standard as part of ensuring accurate, data-driven insights can drive brand decision-making.

Transparency is seen as a sortable problem; brand safety is more of a systemic problem and will require significant and continuous pressure to be resolved.

Most brands’ perception is that their agency is responsible for protecting brand safety and delivering on programmatic transparency, but agencies have been slow to fully understand this responsibility to date. For media agencies, this represents an ideal opportunity to rebuild fractured client relationships.

FOUR: Media measurement is not fit for purpose and is causing a bias of investment

“In digital, clients have learned that audiences are easy to find but attention is not, and quality is re-emerging as a key attribute for them.”

A fractured and non-standardised media measurement ecosystem is an impediment to better communications planning, budget planning and advanced consumer insight.

Media and effectiveness measurement is a source of frustration for marketers. As the number of routes to market continue to proliferate, brands are crying out for unification and integration of their marketing metrics, but the measurement industry remains siloed and increasingly fragmented.

A good case in point is the dramatically different criteria persisting across media channels to determine an advertising impression, which can give a false impression of media efficiency. The “monopoly of the “closed systems” of the big technology platforms are perceived as self-serving and limit how effectively brands can run campaigns across them.

A major issue is bias. The phenomenon where the plethora of digital data and metrics has led paradoxically to a “bias of spend” on channels that provide rich datasets, but without much evidence of real success and effectiveness.

In digital, clients have learned that audiences are easy to find but attention is not, and quality is re-emerging as a key attribute for them. Programmatic media is very efficient for targeting purposes, but targeting alone is no guarantee of marketing effectiveness.

FIVE: We may have reached peak media complexity

For many companies, budget allocation into brand-building and conversion-driving activity is settling down close to a 50/50 ratio. In the paid media channels, we see a similar ratio of spend allocated to digital and traditional media, and within organisations, we see brand and performance marketing spends settling into an equal value share.

Much of the “expectation” created by the availability of automation, dynamic content and social platforms has subsided.

Of course, no brand is the same and no marketing organisation is the same either. But, all organisations are moving (some more quickly and ably than others,) towards data-driven models. Brands now more than ever, have more choice as to how they operate and with whom.

If you would like to know more about how each element can impact your business, and the steps you need to take to ensure you don’t become lost in the ecosystem, get in touch.